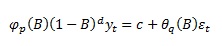

To rewrite it in the form including drift term:

It is implemented that way in R package forecast (Rob J. Hydman). The R implementation has one more catch – the moving average polynomial is defined with a "+" instead of "-":

When d=0, the μ is called “mean”.

When d=1, the μ is called “drift”.

Simple t-test can be used to test for μ parameter significance.

The c constant can be rewritten into μ form:

The μ is the mean of differenced time series (not same as “sample mean” due to autocorrelation).

No comments:

Post a Comment